Open enrollment season is upon us! This is the second in our series of blogs summarizing the material from our #getcovered tweet chat and highlighting important facts about open enrollment. Be sure to check the blogs every Tuesday thru December 5th for great tips and tricks to help you navigate the complicated insurance maze.

Open enrollment season is upon us! This is the second in our series of blogs summarizing the material from our #getcovered tweet chat and highlighting important facts about open enrollment. Be sure to check the blogs every Tuesday thru December 5th for great tips and tricks to help you navigate the complicated insurance maze.

Remember that you can always get more in depth information about insurance via the OncoLink Health Insurance webinar series, available now, www.oncolink.org/insurance. All modules are available to listen to on demand and are free of charge!

During Medicare open enrollment, what changes to my plan(s) can I make?

- You can purchase a Medigap/Medicare Supplemental plan. These plans are offered by private insurance companies. Some employers do offer these for their retirees as well.

- These plans help to fill gaps in coverage, like co-pays and co-insurances, left by Part A and Part B coverage. Remember, Part B only covers 80% of you outpatient charges, leaving you with a 20% responsibility.

- KEY ENROLLMENT FACT: If you are not in your initial coverage period, (the month before, of and after your become eligible for Medicare), these private insurance companies CAN look at pre-existing conditions in their medical underwriting process. As a result, if you have a cancer or other serious diagnosis, your premiums for supplemental plans can be higher if you buy after your initial enrollment period. I usually advise people to buy supplemental coverage as soon as they are eligible to get the best price.

- There are higher premiums for tobacco users with most Medicare supplemental plans.

- You can also change to a different supplemental plan. If you have had continuous coverage from a supplemental plan, the companies cannot employ medical underwriting and charge higher premiums for pre-existing condition. But the key here is CONTINUOUS COVERAGE. You can’t take a break for a year and come back without consequences in the form of higher premiums.

- You can also elect or change your Medicare Part D (prescription drug coverage). Once again, if you didn’t elect Part D coverage during your initial enrollment period, you are responsible for late enrollment penalties. These can add up! Once again, it’s smart to purchase coverage when you are FIRST ELIGIBLE to avoid penalties.

- You can also decide to transition to or switch to a different Medicare Advantage plan during Medicare open enrollment. These plans must offer the same benefits as traditional Medicare A and B, but also tend to bundle in Part D coverage and some plans even include dental and vision benefits. You are essentially, selling your Medicare to a private company to manage. This is easy to do and can offer many benefits.

- But, READ THE FINE PRINT. These plans are hard to get out of once you are in them, especially if you have been in the plan for more than one year. You cannot dis-enroll from Medicare Advantage back to a traditional Medicare plan during open enrollment. There is a special disenrollment period that runs from Jan 1-Feb 14th Remember that you will still need to enroll in a part D plan and purchase gap coverage, but since you are outside of open enrollment AND past your initial coverage period, your premiums for this coverage may be higher.

I have Medicare. Can I buy a plan through the marketplace as a supplement?

- The Marketplace (healthcare.gov) is for individuals who don’t have insurance. You have Medicare, so you have insurance!

- Marketplace plans ARE NOT Medicare supplemental plans.

How does the ACA impact my Part D coverage?

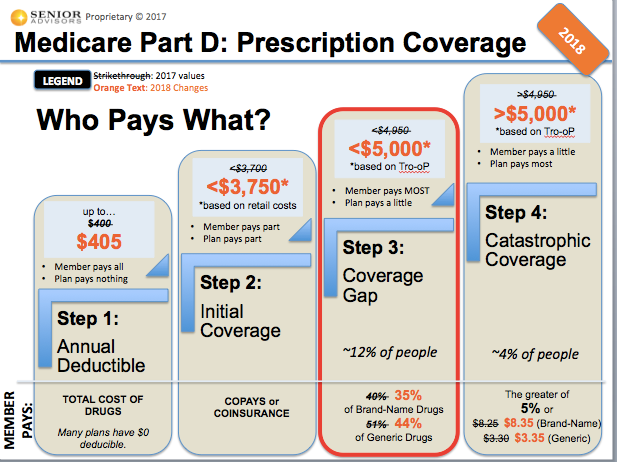

- Yes, the ACA is having an impact on your Part D coverage and out of pocket expenses. Over the years, beginning in 2014, the coverage gap (aka the “donut hole”), the time when you were paying most if not all of the costs of your medications, is getting smaller.

- This is a great graphic showing the breakdown of the Medicare Part D coverage for 2018.

Where can I get information to help me compare plans?

- Use the Medicare plan finder. It can help you identify Medigap/Supplemental, Medicare Part D and Medicare Advantage plans in your area as well as compare benefits across plans.

Next week, we will focus more on estimating and budgeting for health care costs, potential sources for assistance and ACA/Private insurance supplemental options.

Thanks again to Triage Cancer, Young Survivors Coalition, CARIE, NCCS and the National Patient Advocate Foundation for all of your contributions to our Tweet chat and our open enrollment blogs.